How to read a merchant statement, Heartland-style

As a small business owner, time is your most valuable asset. Reading through a merchant statement every month may not seem like a good use of your time. But believe it or not, your statement gives you actionable, easy-to-read data at your fingertips. Each month, you have a peek into how your business is performing – which can help you make money-saving decisions.

At Heartland, we pride ourselves on making merchant statements that are easy to read and most importantly, transparent. We want you to feel confident about your payment processing, without having to decipher lengthy, complicated invoices. Each month Heartland payments customers get a statement at a glance. It’s a straightforward overview that includes the cover page — where you can plainly see fee and deposit totals — and important messages. Heartland merchants can dig a little deeper into the data in their online merchant statement, available through Heartland InfoCentral.

Let’s walk through what you can expect to find on a complete Heartland merchant statement any given month –– to better understand where your money goes and make more informed decisions for your business. Your pricing structure and contract with Heartland will determine what you see on your merchant statement. Ready to learn more? Pick a pricing structure to get the details of what’s covered on that statement type:

Ready for more transparent pricing?

How to read an interchange-plus merchant statement

As an interchange-plus pricing customer, you’ll get a clear picture of what your monthly processing costs are and how you may be able to save down the road. Let’s take a look.

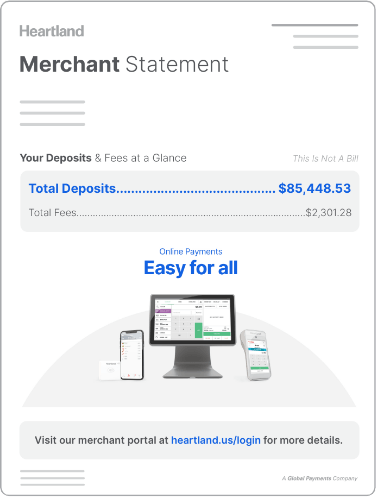

Merchant Statement Cover Page

The big picture

Here you’ll see the entire cost for processing during the month, including total deposits and total fees.

- Total deposits: All the money deposited to your account that month

- Total fees: All fees paid to credit card brands, card issuers and Heartland for processing that month

With this data, you can calculate your effective rate: total processing fees divided by your total deposits (your sales volume during the month). The effective rate is the best way to see the overall percentage you pay for processing and should generally be around three or four percent.

Let’s look at the math for our friendly fictitious merchant, Wally’s Widgets. They had an awesome December thanks to a holiday marketing push:

Total Fees / Total Deposits = Effective Rate

$2,301.28 / $85,448.53 = 2.69%

So for each $1,000 Wally’s deposited in December, they paid $26.94 for processing.

What you can do with this data

Calculating your effective rate can give you a gut check each month on your processing spend. Concerned about your effective rate? Call the dedicated Client Management team to get a better understanding of what’s going on.

Important Messages

The news you need

Get all your Heartland news that’s fit to print each month on this page. We’ll keep you in the loop about changes in the industry, including news related to PCI, EMV as well as interchange adjustments from card brands that could affect your business. We’ll also include any changes to your Heartland account.

What you can do with this

You can take a deep dive into your business' data to see if – and how – upcoming changes could affect you. If you're unsure about anything on this page, you can call the Customer Service number listed on your statement to get answers.

Your Business and Fee Summary

The brass tacks

These sections break down the fees you pay so you know where every penny goes.

Your Business

These handy-dandy graphics show you

- How your sales activity (volume) has changed over the past 13 months

- The card types you accept by sales volume

What you can do with this data

This may help you determine if a surcharge program or PIN debit are good options for your business. Generally speaking, PIN debit transactions are cheaper for merchants with higher average tickets. Signature debit transactions may be cheaper for merchants with lower average tickets.

Fee Summary

Here we go, everyone. Your Fee Summary will always make up the bulk of your statement by far. Why? It lists every single transaction fee that month. Every. Single. One.

Before we translate Wally’s transactions, let’s talk about where each cent in this section goes.

Three main entities collect fees to facilitate the acceptance of credit cards

There may be other organizations collecting fees if you’re using a payment gateway or other third-party service, but the three below are standard. These members of the credit card network charge and collect various fees.

Card brands

Card issuers

Your processor

Banks charge interchange fees to cover transaction processing costs

Now that we know where the cash is going, let’s take a look at the elephant in the room: interchange rates. They determine the interchange fee amount merchants pay to cover the cost of moving a payment transaction through various stages of the authorization network and moving money from one account to another. Interchange rates are:

- Set by the credit card brands

- Non-negotiable for merchants or processors

- Public knowledge – many credit card companies list them on their websites

- Determined by your MCC code

- Generally updated twice per year

Heartland doesn’t receive any portion of interchange fees – which include dues and assessments, discount per item (DPI), and discount % rate fee. Unlike other payment processors out there, we pass through the true wholesale cost to merchants without inflated costs, markup or hidden fees.

Which fees go to who?

Card brands

Dues and assessments

Card issuers (banks)

Discount per item (DPI)

Discount % rate fee

Heartland

HPS processing fees

Your Fee Summary key

We could never list every single card type you’ll encounter in the wild. But here’s a key to help you understand some of what you’ll see when reading your Fee Summary.

Fee type: This is the actual card type you accepted

VS: Visa

MC: Mastercard

DS: Discover

Amex: American Express

DB: Debit cards

CR: Credit card

Anything not ‘CR’ or ‘DB’: Dues and assessments set by the card brand

Discount % rate: This is the percentage paid to the card issuer (banks) to accept each particular card type

DPI (Discount per item): Fee based on the relationship your customer has with the card issuer (bank)

Transaction fee: Most likely, these fall into the category of dues and assessments – and are calculated based on the number of transactions

Bus: Business

Tier: Interchange rates are tiered depending on the type of card used and the method of processing. Generally, the more secure the transaction, the lower the rate. Qualified transactions have the lowest rate, while non-qualified have the highest.

Qualified: debit cards and non-reward card transactions swiped or inserted as a chip Mid-qualified: membership rewards cards, loyalty cards, and manually keyed transactions

Mid-qualified: membership rewards cards, loyalty cards, and manually keyed transactions

Non-qualified: corporate cards, high-reward and international cards, and card-not-present transactions

Level: Levels 1, 2, and 3 refer to the amount of cardholder data that is submitted with an authorization request. The higher the level, the more secure the transaction and therefore the lower the interchange rate. Since Levels 2 and 3 require more data, they generally have lower rates.

How to read a Fee Summary line by line

Let’s go back to Wally’s Widgets’ December statement. Use the key and take a look at the “Visa Pass-thru Interchange & Fees” lines from their Fee Summary.

Mastercard, Visa, Discover and American Express transactions and fees are shown in their own sections under the Fee Summary. Each card has its own discount rate, DPI, and dues and assessments.

What does this tell you about Wally’s December statement?

- Wally’s processed 255 basic Visa debit cards from various banks

- Total Fee = (Total $ Amount x Discount % Rate) + (DPI x # of Trans)

$64.15 = (.0005 x 16,164.58) + (.22 x 255) - Wally’s processed one Visa corporate travel service card this month

- Wally’s Total Fee for that transaction was $21.03 = ($789.60 x .026500) + (1 x .10)

- Wally’s paid a Visa transaction fee for 632 transactions (dues and assessments)

- Wally’s paid a Visa processing fee on 563 transactions (dues and assessments)

If you’re scratching your head at this point, don’t worry. Heartland’s client management team is always here to answer your questions.

What you can do with this data

This information is purely for your benefit. It’s your way to see what you’re paying to the card brands and card issuers. Many Heartland competitors pad interchange with hidden fees and higher rates, so we want you to be able to check every penny if that’s your wish.

To ensure you’re not overpaying, compare your processing statement or rates quote to what's on the card brand websites. Make sure you’re accounting for downgrades, which happen when a transaction is routed to an interchange tier priced higher than the target tier. Downgrades usually reflect a lower level of card data security (i.e., keying in a credit card number instead of swiping it so the L2 or L3 cardholder data is included.) If you’re accruing a lot of downgrades, you’re paying more in interchange fees. Spotting them can help you take action to limit how many you have.

HPS Processing Fees: understanding Heartland’s processing charges

We show what you pay to us for being your processor in its own section called HPS Processing Fees. When your customers pay with plastic, Heartland charges fees to cover the cost of moving your money into your bank account. We typically charge four fees:

- Discount fee: This fee is what Heartland charges to a merchant for passthrough payment processing services to debit and credit card companies.

- Transaction fee: This fee is for the attempt at running a transaction.

- Service and regulatory mandate: This monthly fee pays for some of the things that make the Heartland experience best-in-class:

- 24/7/365 US-based customer support

- Access to Sysnet, our trusted partner for validating your PCI compliance; many of our competitors expect you to find a vendor on your own and that can be expensive

- Enrollment in the Merchant Protection Plan, which covers you up to $100,000 in the event of a data breach

- Access to InfoCentral: an online portal through which you can easily access all of your account data, including batch information and state-of-the-art security features to keep you and your customers’ data safe

- Monthly vs. daily discount cost: Card brands bill and settle processors daily, which can be an overwhelming task for some small businesses. We charge a minimal fee to allow businesses to settle monthly instead.

What you can do with this data

Remember the effective rate we figured at the beginning? You can use this information to calculate your Heartland effective rate so you know the percentage you pay for processing.

Value Added Services Fee Summary

See your extras

This section shows any fees paid for your subscriptions such as Heartland Gift, Customer Intelligence Suite and more.

What you can do with this data

Seeing your monthly subscription costs can help you calculate return on investment (ROI) with any email marketing, gift programs, etc. you may have. Be sure to assess it over a period of time as gift card spending trends fluctuate from month to month.

Processing Summary – Settled by Heartland

Visualize your credit card processing fees

Break down the same data from the “Fee Summary” section by card brand.

What you can do with this data

Scan this section for additional context on whether PIN debit or surcharging would benefit your business.

Processing Summary – Settled by Others

Your third-party transactions

If you require a third party to settle transactions based on your processing method, you’d see those here. You'd also receive a statement from your third-party company.

What you can do with this data

Compare the Heartland statement against your third-party statement to confirm everything is correct.

Deposit Detail

See every single deposit

Break down each deposit based on your batch number, showing fees taken out before the deposit. Whether you deposit daily or monthly may affect what you see. Monthly billing merchants would see that the total deposit and auto-debit/credit amount would be the same.

What you can do with this data

Compare and reconcile your records.

How to read a flat-rate merchant statement

As a flat-rate customer, you probably want payment processing to be as easy and clear as possible. We’ve got you! Your Heartland merchant statement will show you what you need to know about your processing costs.

Like the interchange-plus customer statement, the first two sections of your statement will be a merchant cover page and important messages. That’s where the similarities end. Let’s walk through the statement of a fictitious flat-rate customer, a bakery pop-up called Carli’s Cupcakes.

Processing Summary - Settled by HPS

This section provides you with a detailed breakdown of the types of cards that your business has accepted in the past month. You can see the number of transactions, sales volume, number of refunds, the amount refunded, amount of net sales and the average ticket, all broken down per card brand and type.

What does this tell you about Carli’s statement?

She recorded 26 total transactions this month, equaling a total amount of $756.42 in net sales. She accepted one Visa credit card and 20 Visa non-PIN debit cards, one Mastercard credit card and four Mastercard non-PIN debit cards. Her total average ticket for the month was $29.09.

Processing Summary - Settled by Others

This section provides you with the same detailed breakdown as the processing summary above, but specifically looks at transactions processed outside of Heartland’s network. This comes into play if your business is paying any money to Amex directly.

If you’re hoping to maximize potential sales by accepting American Express but are concerned about the cost, Amex’s OptBlue program allows your processing provider to bundle American Express’ interchange rates with the other cards you accept. Talk to your Heartland representative or call customer service if you’re interested to see if you qualify.

Fee Summary

This is where you can view the fees that Heartland is charging to process your cards.

The fees are broken down by the type of transaction

Card not present (CNP)

Card present (CP)

The transaction type affects what you pay with flat-rate pricing. A card-not-present transaction happens when a customer’s physical credit card or debit card is not actively swiped or dipped by the business — the sale takes place online or over the phone. A card-present transaction happens when a customer uses a physical card at the business. Payment processors, card brands, and issuing banks all know that card-not-present transactions have a greater risk of fraud and chargebacks — that said, you’ll likely pay more for CNP transactions no matter who you process with.

Let’s take another look at Carli’s statement and her processing habits.

You can see a discount rate of 2.90% is charged to the total volume of all card-not-present transactions, and a 2.60% discount rate is charged to the volume of all card-present transactions. CNP transactions are also charged $0.30 per transaction and CP cards are charged $0.10 a transaction. CP cards are charged a lower discount rate and transaction fee because they are considered to be less risky than CNP transactions by nature.

Surcharge Summary

This section highlights information for business owners that participate in Heartland’s card-brand-approved credit surcharge program. Keep in mind that Heartland charges a fee for this functionality, which you’ll see in the Fee Summary (see Carli’s example above).

You’ll see the number of transactions that were surcharged and the total surcharge collected during the past month.

Deposit Detail

This is where you’ll see the total deposits per day in the previous month. This provides you with an extra level of detail to compare to your own records.

Finally, the last page of your statement is typically reserved for any updates from the card brands. This would include increases or decreases of interchange rates, or changes to their incentive programs.

This is great, but my merchant statement doesn’t look like this

Even if you accept card payments with a different processor, we hope we’ve given you a new lens to view your merchant statement through. Your processing statement may look different than Heartland’s –– but the concepts of calculating your effective rate, taking a critical look at your interchange fees to potentially take action –– are all things you can do with your merchant statement today.

It’s easy to get on auto-pilot with your processor –– but your monthly statements tell a tale. Are you listening? Being armed with information can help you potentially save money. You can better evaluate the value of payment processors and payment terminals to make sure you’re getting the most bang for your buck.

You can take action to limit chargebacks, for example. See the impact of accepting EMV chip cards to ensure secure transactions and decrease your fraud liability. (If you don’t have EMV-capable POS terminals, you can get them ASAP. Payment processors also likely offer EMV hardware add-ons at a reasonable cost so you can close the loop on in-person card fraud for customer safety – and lower your processing costs based on the interchange transaction levels.)

The right technology can make a world of a difference in lowering your processing costs, too. When considering a POS, choose a data-centric solution with unlimited fields. Then pack that POS with data, including highly detailed inventory and descriptions, as well as customer and payment data during the purchase. A cloud point of sale makes it easy to access and report on any of this data in real-time from any device, making your team able to quickly and efficiently dispute a chargeback – again, lowering your processing costs.

Could I save money? Should I compare processors? Am I getting my money’s worth – not only in my effective rate but also in my merchant services experience?

If you’re ready to answer those questions for yourself, crack open your merchant statements.

Confidence looks good on you

At Heartland, we value transparency and make it easy to get your questions answered. We like our merchants to feel confident and ready to tackle their business challenges. Our dedicated US-based client management team can walk you through your statement if you have any questions or concerns. Just call our customer service number at 1-888-727-3079.