Heartland is transitioning to the Global Payments brand.

While our logo may change, you'll still get the same hands-on support you know and trust.

While our logo may change, you'll still get the same hands-on support you know and trust.

With transparent pricing, speedy processing and flexible tech, we make sure nothing stops you from improving cash flow and providing an exceptional experience every time customers tap, dip or swipe.

![]()

Whether you have a brick-and-mortar location, an online business or both, you can simplify how you get paid through any channel with a payment service provider built to scale.

![]()

Start accepting payments with peace of mind knowing PCI-compliant encryption, tokenization and secure EMV® tech are working together to protect card data and prevent fraud.

![]()

Payments aren’t complex with Heartland Payments+. Get future-forward POS systems, financial service lending options and seamless integrations for smooth sailing from day one.

Experts predict the digital payments market will grow almost 10% by 2028,1 so now’s the time to invest in solutions that let you securely process any payment method.

![]()

Only 16% of in-store payments were paid in cash in 2023.2

![]()

77% of users prefer credit and debit card payments, making it the number one choice for customers.3

![]()

In April 2023, over 50% of retail payments were made with a smartphone.4 By 2028, the market is predicted to reach about $12 trillion.5

![]()

In 2024, total QR code scans have reached almost 27 million.6

Never turn a paying customer away. Whether in-store, in the field, over the phone or online, you can accept all major credit cards, debit cards, ACH, mobile payments, digital wallets and contactless payments with ease.

Let customers tap, dip or swipe and quickly move on with their day by accepting popular payment methods like Apple Pay® and Google Pay®. You can pick a new payment device or integrate our software with your existing POS hardware.

Make the sale — even if your customer is shopping from their couch after hours — with an online payment processing solution optimized for mobile and popular ecommerce platforms like PayPal®.

Deliver next-level convenience and bring checkout directly to your customers whether they’re curbside, tableside or poolside. With on-the-go processing, you’ll have everything you need to accept payments in a snap.

Speed up your collection cycle, make informed business decisions and put late payments in the past with our AR software.

With flexible payment methods and self-service payment options, you can encourage quick payments and boost days sales outstanding (DSO) averages.

Stop wasting time on repetitive manual tasks prone to human error and focus on high-value work that contributes to the success of your business.

Review financial insights to improve forecasting and plan ahead. With real-time reporting and accurate AR data, you can create clear, money-saving strategies.

Faster funding

Get transactions deposited into your bank account instantly, same day or next day.* You can count on getting your money 365 days a year, including weekends and holidays.

24/7 support

Rely on human customer support from our friendly agents available around the clock — no more navigating aggravating chatbots or confusing forms just to get some help.

Flexible pricing

See your payment processing costs more clearly than ever. Whether you choose flat rate** or interchange plus pricing, we ensure the numbers are clear — so your choice is clear.

Security you can count on

Process with peace of mind knowing end-to-end encryption, tokenization and EMV® technology are working together to protect your merchant account data and shield against fraud.

Never get caught short again. When you batch out using Instant Deposit, the money is available in your checking account in no time.

Schedule recurring deposits, and we’ll transfer the money to your account automatically at the end of the day.

Instant Deposit is available 365 days of the year, including weekends and holidays.

With constant bills coming in and paychecks going out, you can’t afford to wait for slow deposits to hit your account. Say goodbye to waiting — and hello to better cash flow with Instant Deposit.

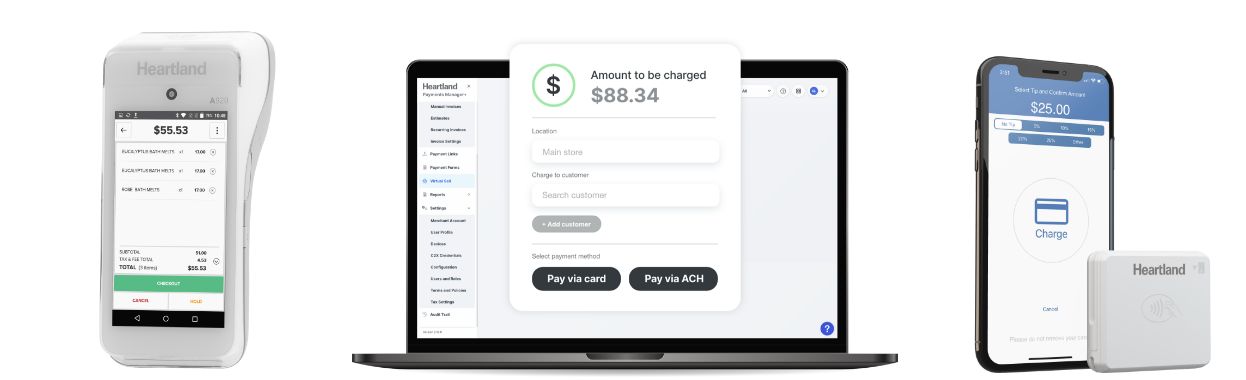

Run your business from the palm of your hand and accept credit card payments from a single device — letting you take your business anywhere.

Turn any device (computer, mobile device or tablet) into a virtual terminal for secure credit card processing during card-not-present transactions. No POS system required.

Process credit and debit card transactions for all the major card brands, including American Express®, Discover®, Mastercard® and Visa®.

Which payment solution is right for me?

It depends on your business size and unique needs. Some businesses, like those operating from a brick and mortar, thrive with a standalone terminal at the counter and some need a point of sale with menu items or inventory management capabilities. Some make online sales only and others need to accept payments in the field or all of the above. No matter what you need — we got you covered. Your Heartland rep will ask you a series of questions about how you conduct business so we can match the right solutions to your business.

Do you have a surcharge or cash discount program?

Yes and yes! Our cash discount not only rewards your cash-paying customers, it also saves you money with zero interchange fees on cash transactions. We support surcharging on many of our payment devices. Our compliant surcharge program enables you to surcharge up to 3% on credit card transactions to help offset your card processing fees.

What kind of support is available?

When you’re open, we are too. We offer 24/7 customer service with English and Spanish-speaking specialists. We also have technical support experts available from 8 am to 9 pm EST should you need assistance with any hardware.

What kind of security do you offer?

We utilize end-to-end encryption technology, which immediately encrypts credit and debit card data as it is captured. We also lock down stored data with tokenization technology, which replaces card data with “tokens” — removing sensitive credit card information as it is passed through the card networks.

How can I get started?

Getting started is easy — if you are already speaking with a Heartland rep, they will direct you through the sign-up process. Or, simply complete this form to self-enroll.

If you've done any research into the tech your business needs to thrive, you've likely run into the word "integrated." But what does that mean for you, your customers and your employees? And is working with one provider for all of your needs the best way to go? Let's break it down.

Without taking advantage of modern tech, your business could be left behind. Learn five ways your payment processing partner can help you grow, from customer intelligence and data analytics to powerful people management.

There's a lot that goes into choosing a payment processor. We've compiled a list of questions that can help you get the info you need to make an informed decision before signing a processing agreement.

1www.statista.com/outlook/dmo/fintech/digital-payments/worldwide

2www.frbservices.org/news/press-releases/051324-findings-from-diary-of-consumer-payment-choice-increased-payments

3www.connectpos.com/top-5-payment-methods-that-pos-should-support/

4www.businesswire.com/news/home/20231031392228/en/Global-POS-Payment-Methods-Analysis-Report-2023-2027-Landscape-is-Expected-to-be-Dominated-by-Mobile-and-Contactless-Card-Payments-Particularly-in-the-U.S.-Germany-and-China---ResearchAndMarkets.com

5moneytransfers.com/sending-money/mobile-money/mobile-payment-statistics

6www.qrcode-tiger.com/qr-code-statistics-2022-q1

*Merchants on certain processing programs are not eligible for next-day funding; funding may be delayed by Heartland Credit or Risk departments at any time. **Not all merchants or transactions will qualify for flat-rate pricing; additional fees may apply. Increases in assessments by card associations may apply. †Surcharging is prohibited in some states and merchants are responsible for complying with all applicable laws.